Introduction

LCCA as a Decision-Making Process

LCCA Inputs

Environmental and Social Considerations in LCCA

LCCA Analysis Methods

LCCA Case Study

Interpretation and Implementation of LCCA

Summary and Conclusions

Introduction

Life Cycle Cost Analysis (LCCA) is used in our daily life to make simple decisions and in the selection of best alternatives in complex infrastructure projects. Regardless of the applications of LCCA, at the end of this process, someone must select the best alternative based on this tool. In this paper, applications and challenges in the application of LCCA for transportation infrastructure projects and more specifically for roads and pavements will be investigated. In many cases, organizations and their engineers conduct LCCA to support and justify their decisions. However, the accuracy and reliability of LCCA outputs depend on many parameters.

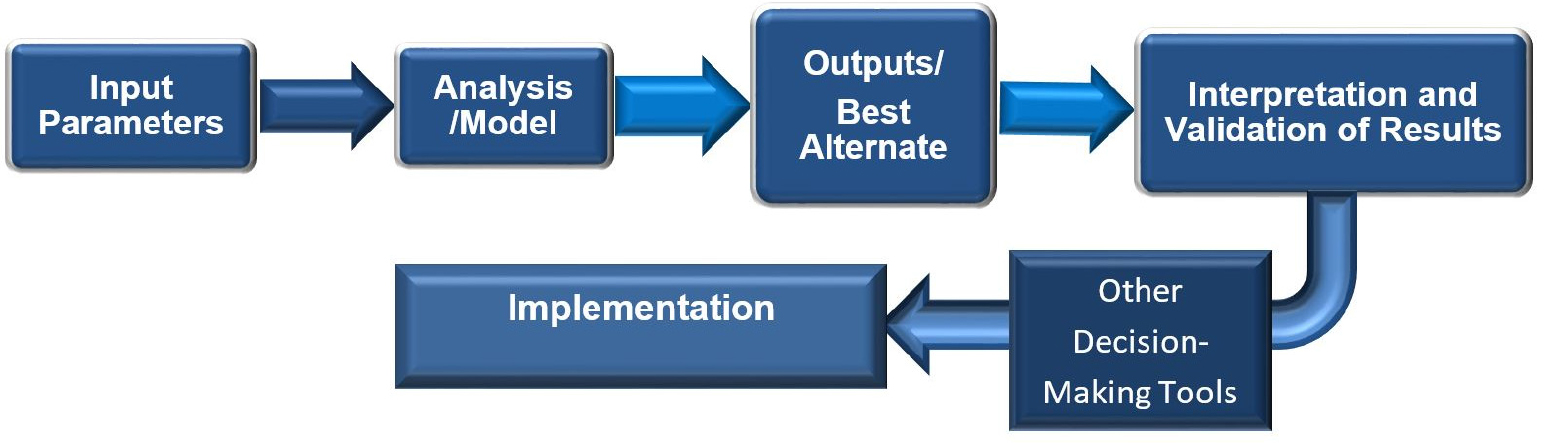

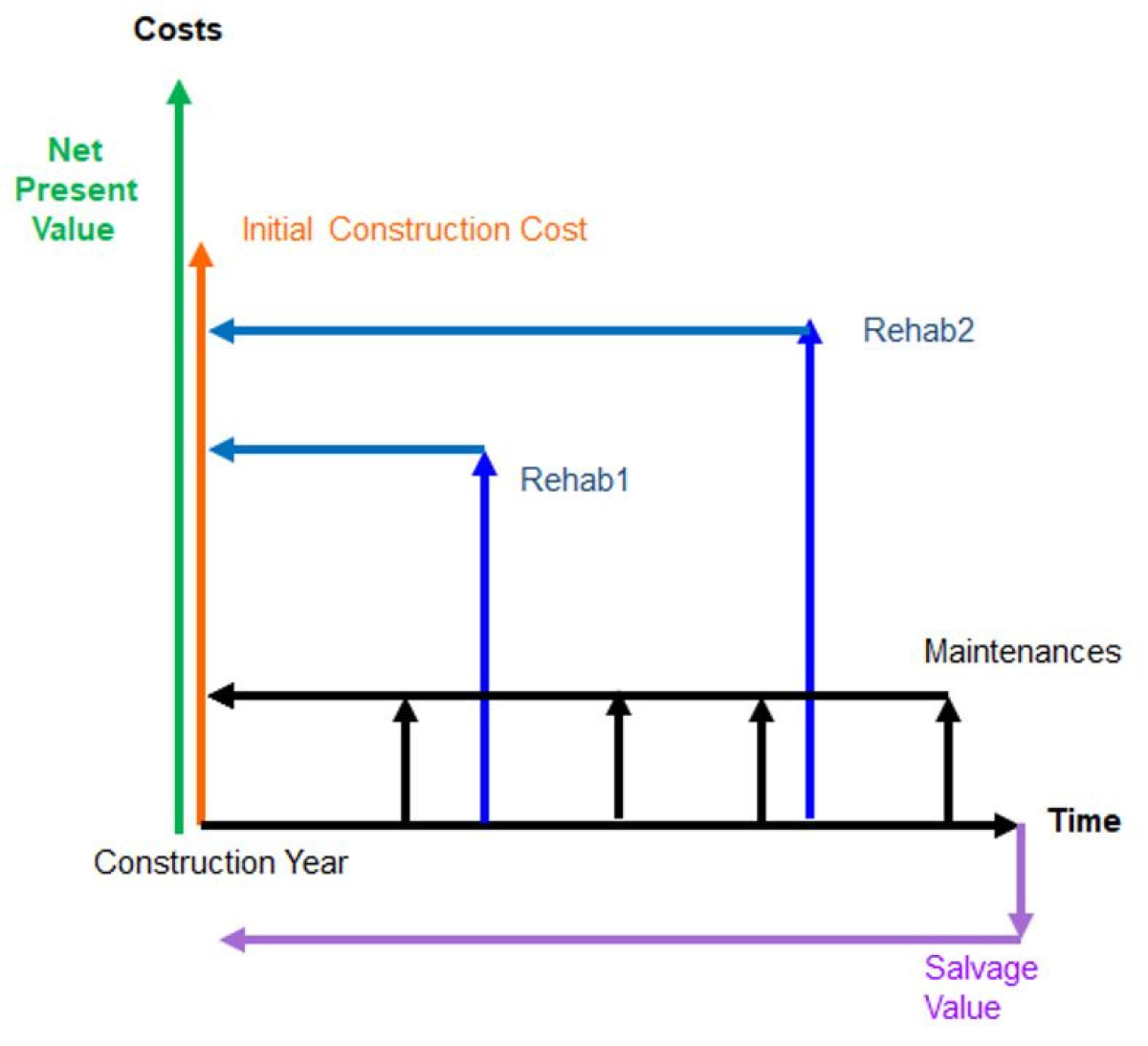

A simple model of LCCA is shown in Figure 1. As it can be seen in Figure 1, a LCCA includes input parameters, an analysis method or model, and outputs or ranking of several alternatives. An important step that must be considered is interpretation or validation of results before implementation of LCCA outputs.

LCCA as a Decision-Making Process

LCCA can be used for different infrastructure projects such as buildings, bridges, dams, pipelines, pavements, sidewalks, and other assets that their owners or designers should select the best alternative from several options. In the pavement engineering area, LCCA can be applied for the selection of pavement structure for new roads or it can be applied to pavement maintenance and rehabilitation projects to select the best road treatments.

LCCA can be conducted at different stages of a project. For example, it can be used in the planning, design, maintenance, and rehabilitation of an asset. In most infrastructure LCCA projects, it is expected to look at the Whole Life Cycle Cost (WLCC) which includes initial construction costs, costs and times of required maintenance and rehabilitations, and even disposal of the asset. The definition of “whole” in a WLCCA could be different in different industries, for example, in pavement engineering, one common concept of “whole” could be incorporation of all important factors such as energy consumption related to extraction and production of materials, CO2 generation from all project’s activities, and social costs such as users’ delay and even cost of accidents. Incorporating environmental and social costs in an infrastructure project is a challenging task in LCCA as will be explained more in the next sections.

LCCA Inputs

The most important input parameters in any LCCA are costs and service lives of different alternatives. This looks a simple task; however, it will be a complex process for major projects and requires comprehensive investigation and research to find accurate costs and service lives of different materials or alternatives. Initial costs are the highest and most important input parameter which will impact the LCCA results more than the future project’s costs. Some agencies consider the initial project costs as the only project’s cost. This approach might work for some assets when future costs of the project are relatively low; however, for long-term projects that have high maintenance costs, it is not the best methodology. For example, in the selection of best surfacing material (asphalt vs concrete) for a paving project, if only the initial cost is considered, asphalt pavement must be selected for all projects as the initial cost of concrete could be 3 to 4 times more than the initial cost of asphalt; however, if the cost of required maintenance and rehabilitations during the life of a rod are considered, results could change. Municipal agencies use concrete paving for their bus stops or at their intersections as the maintenance cost of asphalt paving is very high at these locations.

Most agencies use their historical bid data, averages of the last 3 or 5 years, as the cost of their future projects. Cautions must be taken in using historical bid data as many factors such as size and location of the projects, inflation, and local and global events can change the future initial costs. One example of cost change in pavement area was when the price of oil reached above $100 in 2010 to 2014, the cost of paving with asphalt mixes increased, while the cost of Portland cement was relatively stable during the same time. Consequently, the gap between initial costs of paving with asphalt mixtures and concrete reduced significantly. This changed the previous results of LCCA of agencies that historically used asphalt, as their preferred paving material, to concrete paving. It is expected that the recent supply chain issues and higher price of oil in 2022 have similar impacts. In these conditions previous LCCA results must be revised.

In some cases, project costs are divided into direct and indirect costs. For example, in a paving project, agencies’ costs such as initial construction and future maintenance costs are considered as the direct costs but other costs such as energy consumption, CO2 generations, and road users’ delays are treated as indirect costs. In most cases, only direct costs are considered in LCCA. Results of LCCA can change significantly when indirect costs are included.

Size and productivity of paving projects will impact their initial and maintenance costs. Typical highway paving projects require higher quantities of materials than municipalities’ paving projects. For two similar projects, for example, one km of a new paving project with the same construction material, construction costs are significantly lower for highway agencies than municipalities as the productivity of contractors is significantly less in urban areas than the rural areas. Therefore, LCCA results from one agency should not be used by another agency except that all input parameters have been verified.

Frequency, timelines, and type of infrastructure maintenance or rehabilitations are difficult to determine due to many unknowns. As a general rule, the earlier costs for an asset, it will impact the LCCA results more than the subsequent costs. On the other hand, most infrastructure projects require more frequent maintenance as they age. To simplify the process, if the operational costs are similar for different alternatives, they have no impact and can be eliminated; otherwise, they must be included in LCCA.

Another factor in any LCCA is to estimate the service life of different materials and alternatives, during the projects’ life. These parameters are difficult to estimate accurately as they depend on many attributes. In pavement projects, service life is defined from the time of initial project’s completion until the time that road requires a major rehabilitation. It is expected that a road experiences several rehabilitations during its life. Maintenances are the required regular and seasonal activities to provide safety to road users immediately after project operation. To accurately estimate the type and time of maintenance and rehabilitation for specific project alternatives, the agencies’ historical information and more specific pavement deterioration curves from pavement management system must be used. Generally, in a LCCA for roads, rehabilitation costs have a higher impact than maintenance costs. Therefore, more attention must be applied in the estimating of rehabilitation costs and their times.

The asphalt industry emphasizes on several factors such as the lower initial costs, faster construction, less CO2 generation, and full recyclability of asphalt pavements as advantages of asphalt paving that must be considered in LCCA. On the other hand, cement and concrete industries stress on higher life (typical 40 years for concrete versus 20 years for asphalt), less road closures, less rolling resistance, and fuel efficiency of concrete pavement as its LCC advantages.

Some infrastructure projects such as bridges and pavements are more sensitive to climatic factors. Recent unexpected climatic events such as heat waves and higher precipitations make historical service life trends less accurate. It is expected that in the future, higher moisture and cycles of freeze and thaw reduces the life of pavement and bridges and consequently, more maintenance and earlier rehabilitation will be required.

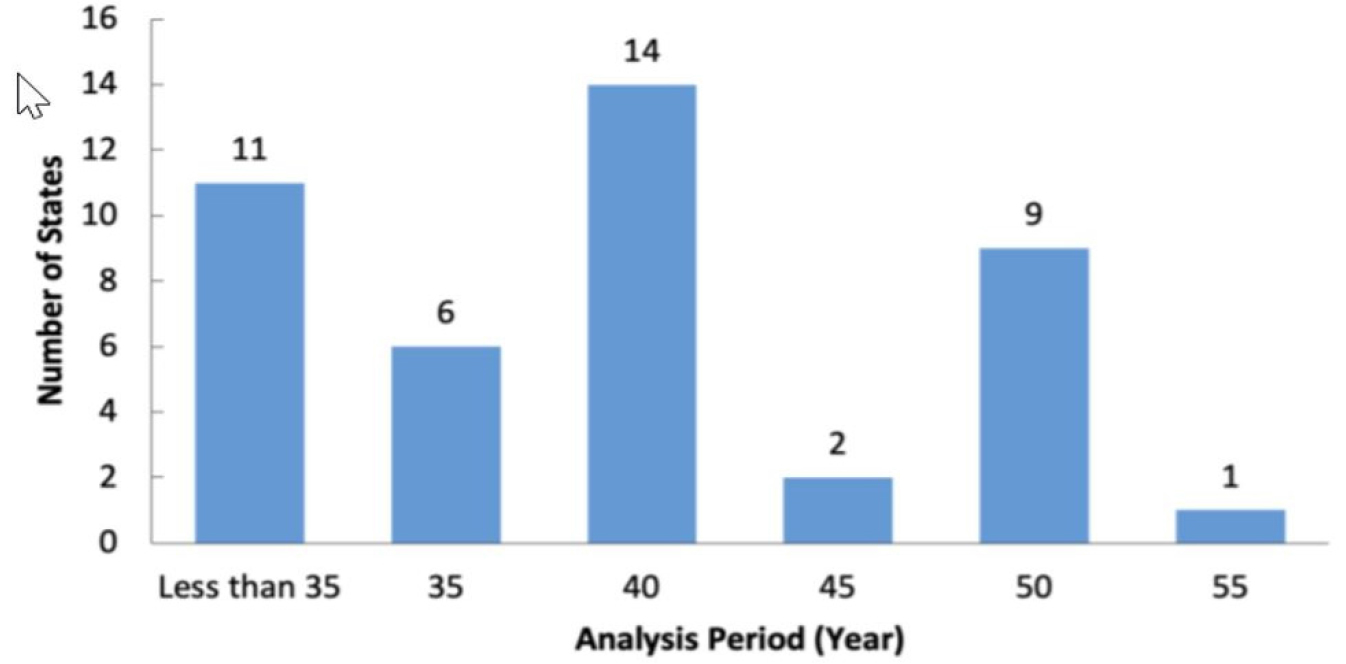

Another important input in a LCCA is the Analysis Period (AP) which must be decided for infrastructure projects. Results of LCCA can change if different APs are considered for the same project. One important consideration in the selection of AP for pavement projects is to include at least one or two major rehabilitations and even project disposal, if it is known. While asphalt and concrete pavements are generally designed for 20- or 30-years life, the AP for them could be 50 to 70 years respectively. AP must be fixed for different alternatives in a LCCA. Figure 2 shows the results of a survey from USA highway agencies for estimating AP for their LCCA of their asphalt pavements [1].

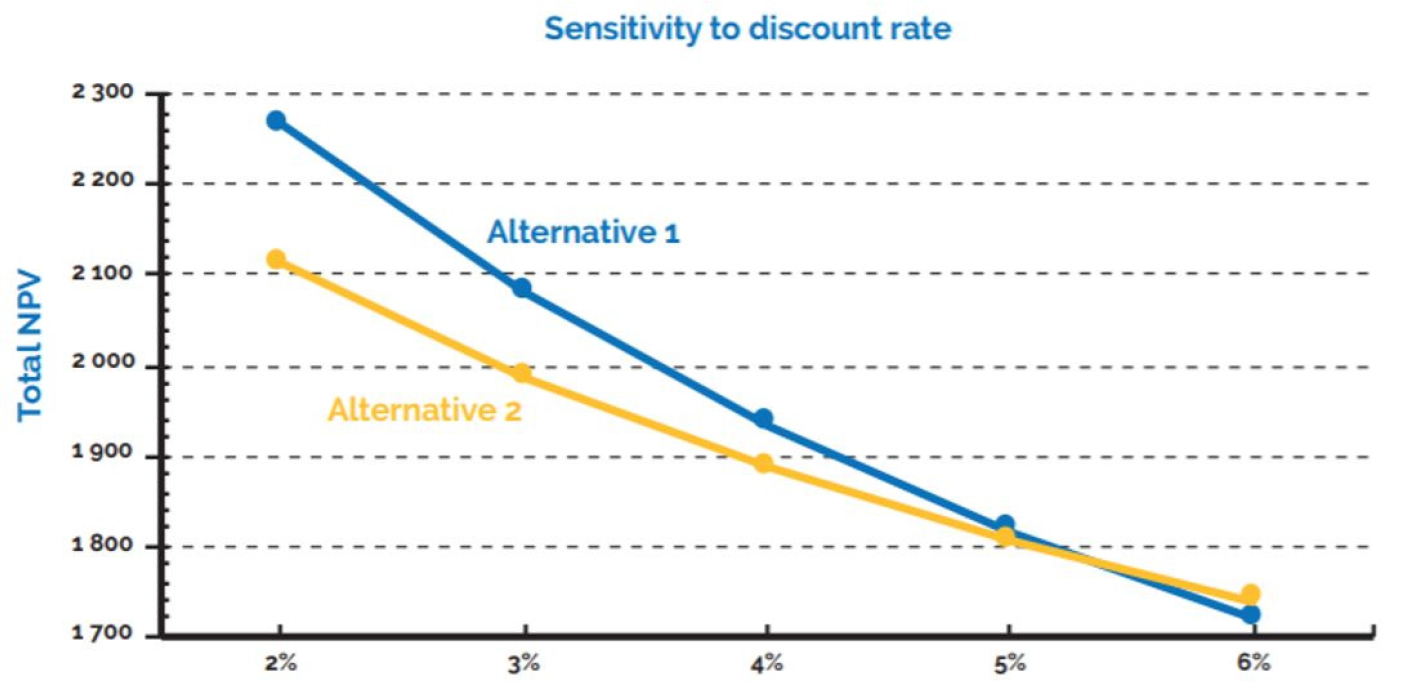

The other important input parameters that must be decided in a LCCA are the future value of money (discount rate). Some general guidelines have been proposed by industry for the inflation rate (around 2 to 4%) in pavement areas. These values are more realistic in normal inflation conditions; however, it could be higher during high inflation times. Figure 3 shows the impact of the discount rate on results of LCCA for two project alternatives [2].

The Salvage value of an asset is used in some LCCA analysis; however, as it happens at the end of the AP, the impact of it on results of LCCA could be negligible.

Environmental and Social Considerations in LCCA

New regulations and requirements demand more sustainable construction materials and practices in infrastructure projects; therefore, agencies require quantifying and incorporating Greenhouse Gases (GHG) emission, social, and users’ costs in their LCCA. This makes the LCCA process more complicated and sometimes biased. It is possible to find literature and studies with different results when these factors have or have not been included in a LCCA.

To consider embodied emissions in a WLCCA of infrastructure projects, all carbon and other emissions during materials extraction, processing and manufacturing, transportation, installation, and placing must be included. This is a difficult task and, in most cases, not practical.

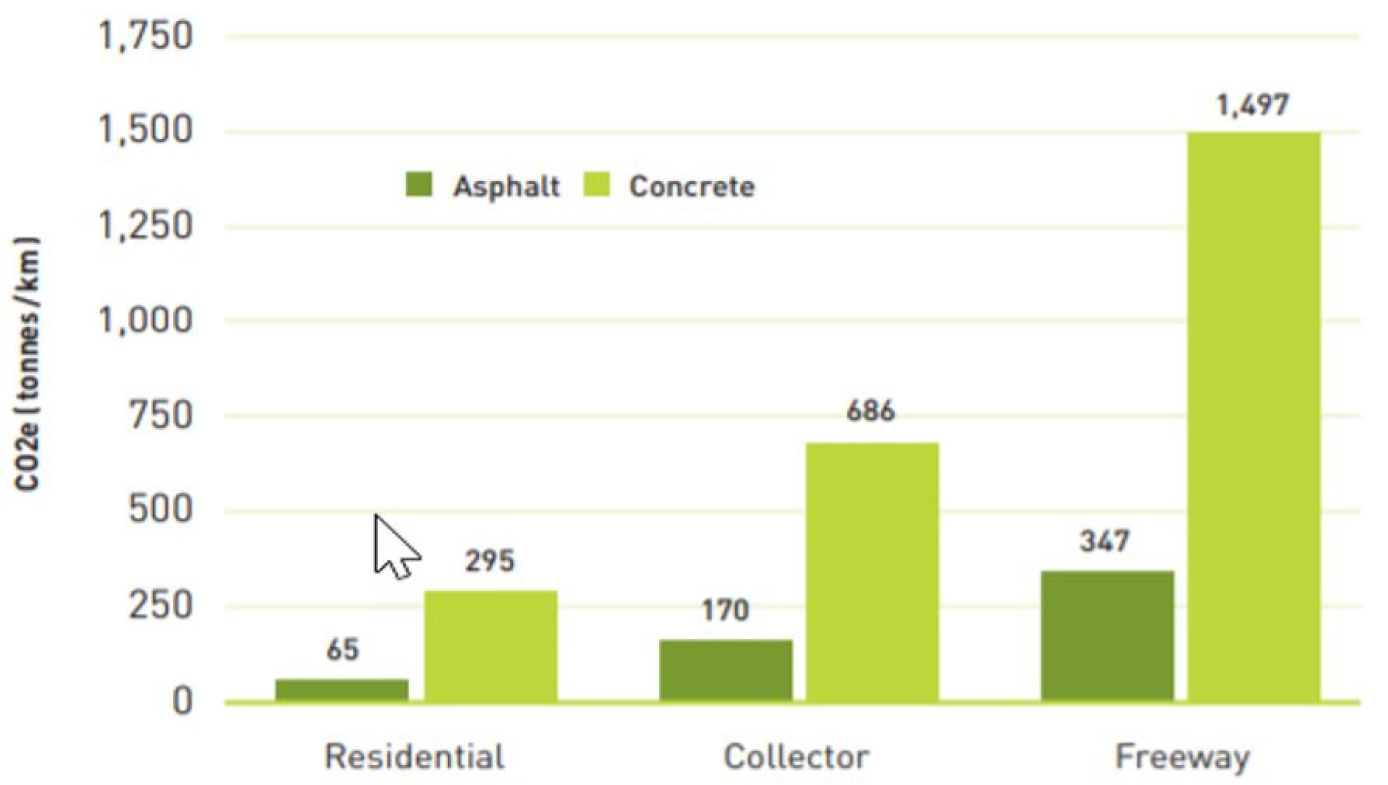

Figure 4 shows typical CO2 footprint values from initial paving of one kilometer of concrete and asphalt pavements for residential, collector, and freeway pavements constructed in Ontario, Canada [3].

Figure 4.

CO2 Generations from Initial Paving of Asphalt and Concrete pavements in Ontario, Canada [3].

Of all construction materials, Portland cement has the highest carbon footprint as it generates twice as much reinforced steel and more than 100 times of aggregate production. A tonne of Portland cement generates approximately 700 to 1000 kg of CO2. This means that a typical cement plant produces around 700 to 1,000 M tonne CO2 annually. Concrete and cement industries are working industriously to reach net zero carbon footprints until 2050. Several tasks that the cement industry is working to achieve this important goal are: more applications of Portland Limestone Cement (PLC), carbon capturing from cement production, using renewable fuels, and more concrete recycling [4].

In a detailed consideration of environmental costs, not only generation of CO2, but also other GHG emissions must be included which makes a WLCCA very complicated. To consider GHG emissions in a LCCA, they must be converted to projects’ costs at different stages of a project. In Canada, the federal price of carbon tax started at $20 per tonne in 2019 and will increase to $170 in 2030 [5]. Example of GHG emission quantification for typical pavement projects in China reported by Feng et al. and Zheg et al. [6, 7].

Uhelman et al. conducted an Eco-Efficiency Analysis (EEA) study for BASF to evaluate the life cycle cost and environmental impact of several road treatment methods for urban roads. The customer benefit applied to various alternatives for an urban road to a similar profile and performance using best engineering practices over a 40 year period. Based on these considerations, some road treatment methods showed almost 45% less CO2 compared to other methods [8]. Foth and Berthelot quantified the whole CO2 generation for different pavement treatment methods. It was shown that the average CO2 generated by one method was almost 17 times more than another road treatment [9].

These and similar studies will help to incorporate energy and GHG emissions’ costs in the LCCA. Results of LCCA can change significantly when these factors are or are not considered in a LCCA for a paving project.

Estimation of social and user costs for an infrastructure project is another challenge in a LCCA and in most cases they are ignored. A Federal Highway Administration (FHWA) publication provided some guidance on how to consider users’ costs for pavement projects [10]. Users’ delay costs due to road closure during any maintenance and rehabilitation of bridges and roads could be estimated for a project. For example in the selection of asphalt or concrete pavements, asphalt pavement is expected to have more maintenance and rehabilitation than a concrete pavement. This is one reason that some highway agencies prefer to use concrete pavement for their high traffic roads to reduce the required road closures and to minimize the users’ costs.

Some social costs like traffic accidents, noise and air pollution are very difficult to quantify in LCCA; therefore, most agencies do not consider them in their LCCA.

LCCA Analysis Methods

After determining the initial, maintenance, and rehabilitation costs and their timelines, a method of analysis must be selected. Some LCC analysis methods are Benefit/Cost ratio (B/C), Net Present Value (NPV), Internal Rate of Return (IRR), and Uniform Annualized Cost Method (UACM). NPV method has been used for many infrastructure LCCA including pavements. Several computer programs, based on different analysis methods, have been developed for LCCA. These methods and their advantages and disadvantages have been explained in detail in the literature [11, 12]. New trends in LCCA methods and software use neural networks and fuzzy logic [13]. It is expected that Artificial Intelligence (AI) will be used in the future as more data is collected from different infrastructure projects [14].

Figure 5 shows graphically a NPV process for one alternative. All considered costs with their expected activity times during the project’s AP are converted to today’s money by applying a discount rate to estimate NPV for each alternative. A simple factor, [] is applied to each future cost to convert them to Present Values. In this converting factor, r is the discount rate and n is the time of project activities. For example, an estimated future cost of $1,000 in year five with a discount rate of 4%, has a NPV of $822, but will be $675, if the same cost occurs in year 10 of the project. When the NPV of each alternative is determined, it is possible to calculate a UACM for them.

One common question is if the inflation rates must be applied to each future cost of alternative? As prediction of future inflations, during AP in a LCCA, is not possible, the future costs are estimated based on today’s costs.

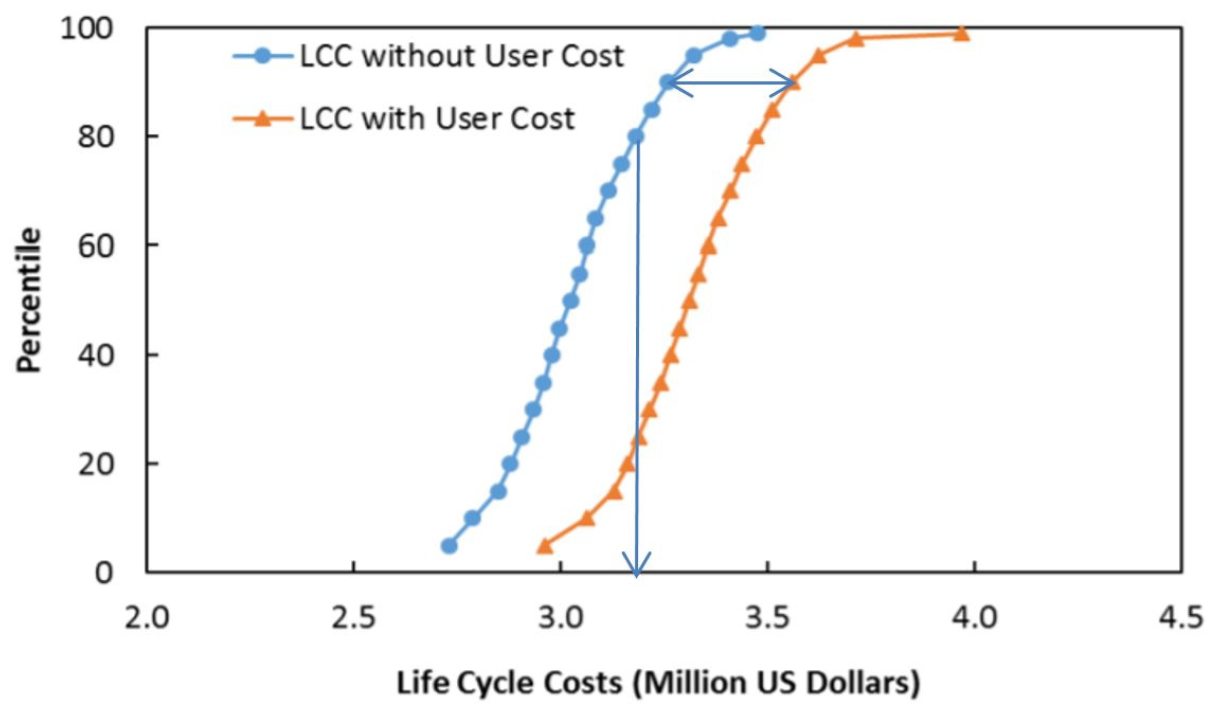

LCCA analysis methods are classified into deterministic and probabilistic methods. In a deterministic LCCA method, average values of input parameters are considered as the best estimate of them. Using a LCCA method, the output also will be a value for each alternative. As it was discussed before, it is difficult to estimate only one value for LCCA costs and their timelines; therefore, considering a range for each project’s costs and activity times could provide various scenarios for LCCA results. Probabilistic methods, using different computer algorithms, consider a range of values and distribution shapes for each input parameter. Therefore, the output is not a fixed value, but a range of possible scenarios which provides a better tool for the decision maker. Figure 6 depicts a LCCA output for two different scenarios, with and without users’ costs for a typical pavement project (2). Parameters such as the difference in NPV at specific cumulative probability and difference in probabilities at specific NPV, from probabilistic results, can be used for comparison between alternatives (for example 90% probability and $3.2 M NPV in Figure 6).

LCCA Case Study

To show subjectivities in LCCA results, two case studies are shown from literature. One related comparison between selection of asphalt or concrete for a new road construction. The objective of this comparison is not to say which one is right or wrong, but to show that results of LCCA can change by considering different assumptions.

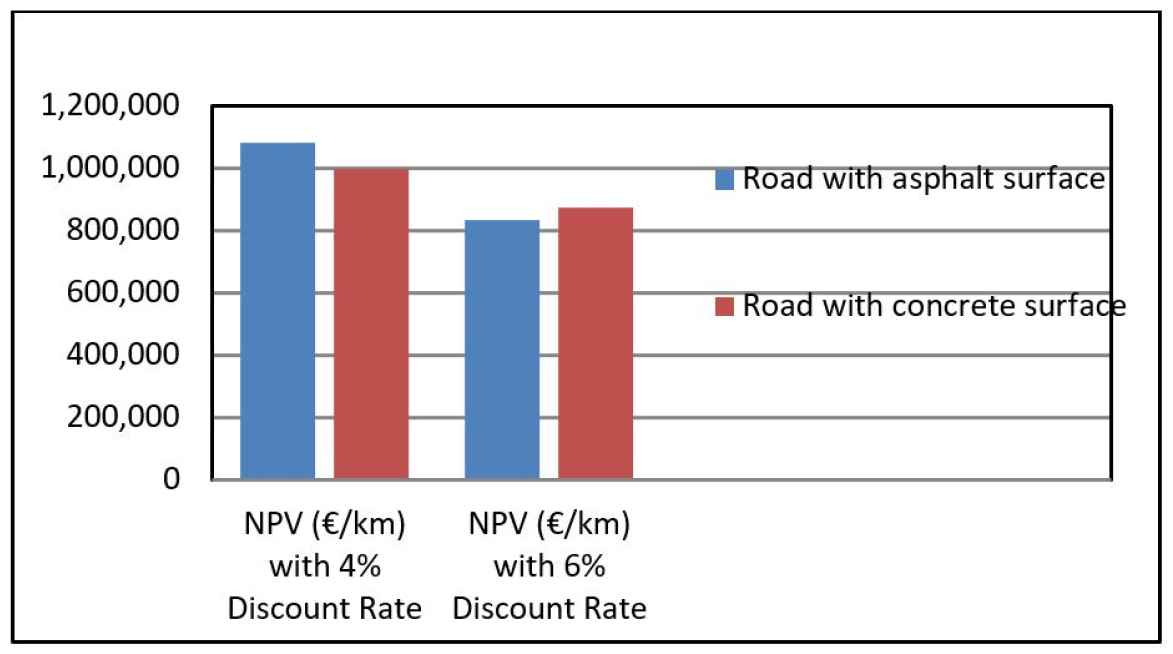

The first study published by the European Concrete Paving Association (EUPAVE) considered two typical pavement structures paved with concrete and asphalt surfaces. A LCCA was conducted for these two alternatives with a discount rate of 4% and 90 years AP and different assumptions for type and time of maintenance and rehabilitation. Results of NPV from this study are shown in Figure 7. Based on this study a road with concrete surface will be approximately 8.5% less costly than a road with asphalt surface during its life (90 years) with a discount rate of 4%; however, when the discount rate increased to 6%, asphalt alternative was approximately 5% less costly. This study did not consider any GHG and users’ costs [15].

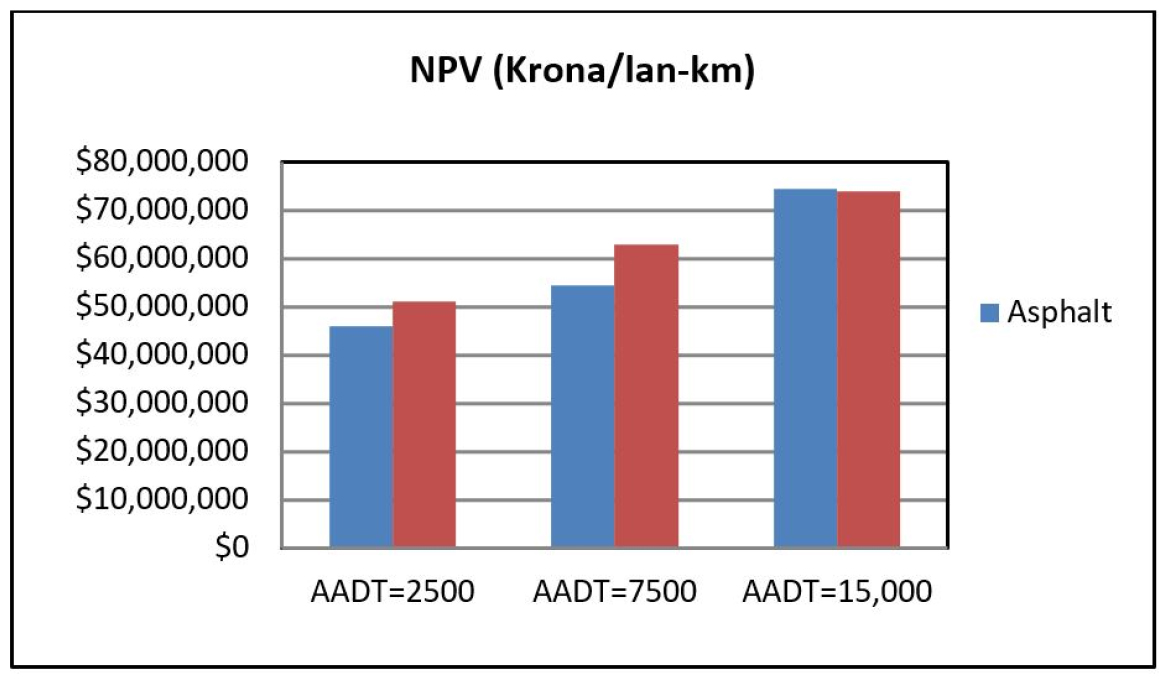

Another European study by Scheving compared the NPV of asphalt and concrete roads in Iceland for different traffic levels. For this comparison, an AP of 40 years and discount rate of 6% were considered. Results are shown in Figure 8. Based on this LCCA, at traffic below 14,000 AADT, concrete pavement was 10% to 15% higher than asphalt; however, concrete was competitive when traffic was higher than 14,000 AADT. This study did not look at any environmental costs, but included the users’ delay costs [16].

Interpretation and Implementation of LCCA

There are subjectivities and uncertainties in any LCCA that a designer must be careful about. Some considerations in the application of LCCA for infrastructural projects are summarized below:

⦁The source, accuracy, and reliability of input parameters must be verified.

⦁Generally, more efforts must be made on accurate estimation of higher and earlier costs as they impact the results more.

⦁Historical costs and past performance experiences of agencies could be considered in LCCA processes; however, they must be reviewed and revisited frequently to reflect the real world conditions.

⦁Probabilistic LCCA models provide a better view of various scenarios for projects’ alternatives than deterministic methods.

⦁Biased or predetermined decisions must be identified and prevented in any LCCA.

⦁Agencies must develop a guide or manual for their LCCA to provide consistency in their LCCA applications.

⦁If LCCA results of various alternatives are very close, other factors such as lower initial cost or shorter construction time can be considered as the best alternative.

⦁In addition to LCCA results, other project management considerations such as risk evaluation, quality control and assurance, complexity of alternatives, project’s delivery and payment methods, and performance-based construction specifications must be considered in the selection of the best projects’ alternatives.

Summary and Conclusions

LCCA is a decision supports tool that prioritizes different alternatives for infrastructure projects. Selection and accuracy of input parameters are important steps in conducting a LCCA. The new trends in transportation infrastructure is to consider environmental and social and users’ costs in LCCA. Challenges in considerations of environmental impacts and user costs for pavement projects were discussed. This paper attempted to review important factors in LCCA and to bring attention to subjectivities and uncertainties in LCCA.